No Signup Required • Instant Results • 100% Free Tools

Debt Snowball Calculator

Use this Debt Snowball Calculator to apply the snowball method and create a clear debt payoff plan. Enter your balances, minimum payments, and extra amount to see which debt to focus on first and how to build momentum over time.

What Is the Debt Snowball Calculator?

The Debt Snowball Calculator is a simple tool that helps you organise and pay off your debts using the debt snowball method.

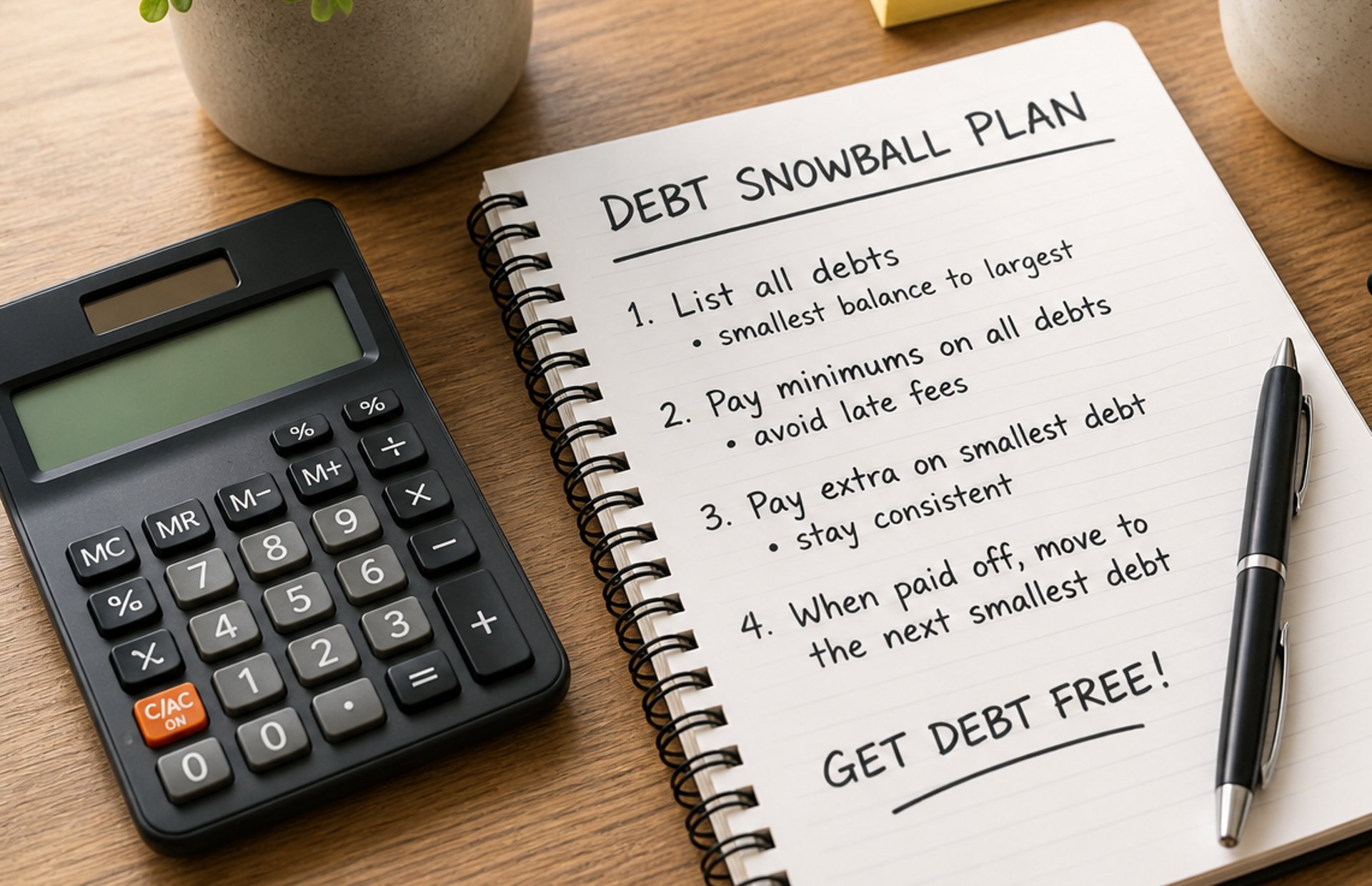

This method focuses on paying off your smallest balance first, while continuing minimum payments on your other debts. As each debt is cleared, the amount you were paying is rolled into the next one — creating a “snowball” effect that builds momentum over time.

Instead of feeling overwhelmed by multiple debts, this calculator gives you a clear payoff order and helps you stay focused on one step at a time.

By entering your balances, minimum payments, and any extra amount you can afford, you can see:

Which debt to pay off first

How your payments grow over time

A simple plan to work toward becoming debt-free

How to Use This Debt Snowball Calculator

Using the Debt Snowball Calculator is simple. Follow these steps to create your payoff plan:

1. Enter your debts

Start by listing all your debts.

Add each one using:

Debt name (e.g. credit card, personal loan)

Balance

Minimum monthly payment

👉 Tip: Enter them from smallest balance to largest for best results.

2. Add more debts if needed

Click “+ Add Another Debt” to include all your accounts.

Make sure everything is listed so your plan is accurate.

3. Enter your extra monthly payment

Add any extra amount you can pay on top of your minimum payments.

Even a small amount like $20–$50 can help you pay off debt faster.

4. Click “Calculate Snowball Plan”

The calculator will:

Organise your debts in the correct order

Show which debt to focus on first

Estimate how long each debt will take to pay off

5. Follow the plan

Start by:

Paying minimums on all debts

Putting extra money toward the smallest debt

Once that debt is paid off:

👉 Roll that payment into the next one

This is how the snowball effect builds momentum.

💡 Tips for Better Results

Be consistent with your payments

Avoid adding new debt while paying off existing ones

Increase your extra payment when possible

Celebrate small wins to stay motivated

Pros and Cons of the Debt Snowball Method

Pros

Easy to follow and understand

Quick wins keep you motivated

Builds momentum over time

Helps reduce overwhelm

Cons

May not save the most on interest

Larger debts can take longer to tackle

Requires consistency to work

Is the Debt Snowball Method Right for You?

The debt snowball method isn’t about being perfect — it’s about staying consistent. But like any strategy, it works better for some people than others.

👍 This method is a great fit if:

You feel overwhelmed by multiple debts

You struggle to stay motivated with long-term plans

You want quick wins to keep you going

You prefer a simple, easy-to-follow system

Focusing on your smallest debt first can give you a sense of progress early on, which makes it easier to stay consistent.

⚖️ You might find it less suitable if:

You want to save the most money on interest

You’re comfortable following a more technical strategy

You don’t need motivation to stay on track

In this case, the debt avalanche method (paying highest interest first) might be a better option.

💡 The bottom line

The best method isn’t the “perfect” one — it’s the one you can stick with.

If staying motivated is your biggest challenge, the debt snowball method can be a powerful way to build momentum and finally make real progress toward becoming debt-free.

FAQ

What is the debt snowball method?

It’s a debt repayment strategy where you pay off your smallest balance first while making minimum payments on other debts.

Does the debt snowball method really work?

Yes. It works well because it builds motivation through quick wins, making it easier to stay consistent.

Is the debt snowball better than avalanche?

Snowball is better for motivation, while avalanche is better for saving money on interest.

How much extra should I pay each month?

Any extra amount helps. Even small payments can build momentum over time.

Can I use this method with low income?

Yes. The method works with any budget — consistency matters more than how much you pay.

Our Services

Tools designed to help you make clear financial decisions daily.

Personal Loans

Estimate repayments, interest, and total costs before you borrow.

Track your balance, reduce interest, and pay off your debt faster.

Credit Cards

Car Loans

Calculate your monthly car payments and plan your budget with confidence.

ClearEveryday

Free Loan & Debt Repayment Calculator

Estimate monthly payments, interest costs, and payoff timelines in seconds.

Link

© ClearEveryday 2026. All rights reserved.

About

For informational purposes only — not financial advice