No Signup Required • Instant Results • 100% Free Tools

Why Minimum Payments Keep You in Debt (And How to Break Free)

Discover why credit card minimum payments keep you in debt and how to pay off your balance faster. Learn strategies and use our free calculator.

CREDIT CARD STRATEGIES

Rachel

3/31/20262 min read

Still in debt even though you’re making payments every month?

You’re not alone — and the problem is usually minimum payments.

While paying the minimum keeps your account in good standing, it can also trap you in long-term debt due to high interest and slow balance reduction.

In this guide, you’ll learn:

Why minimum payments keep you stuck

How interest works against you

What you can do to get out of debt faster

What Is a Minimum Payment?

A minimum payment is the smallest amount you’re required to pay each month on your credit card.

It’s usually based on:

A percentage of your balance (1%–3%)

Interest charges

Fees

👉 It’s designed to keep your account active — not to help you get out of debt quickly

Why Minimum Payments Keep You in Debt

1. Most of Your Payment Goes to Interest

When you carry a balance, interest is added every month.

So when you make a payment:

A large portion goes to interest

Only a small part reduces your actual balance

👉 That’s why your debt barely moves.

2. Your Balance Decreases Very Slowly

Even if you pay every month:

The balance drops little by little

Interest keeps adding back

Example:

Balance: $5,000

APR: 18%

Minimum payment: ~$100

👉 It could take 10+ years to fully pay off

3. You Pay Thousands More Over Time

Minimum payments may feel easier now, but they cost more later.

You stay in debt longer

You pay significantly more in interest

Your total repayment can double

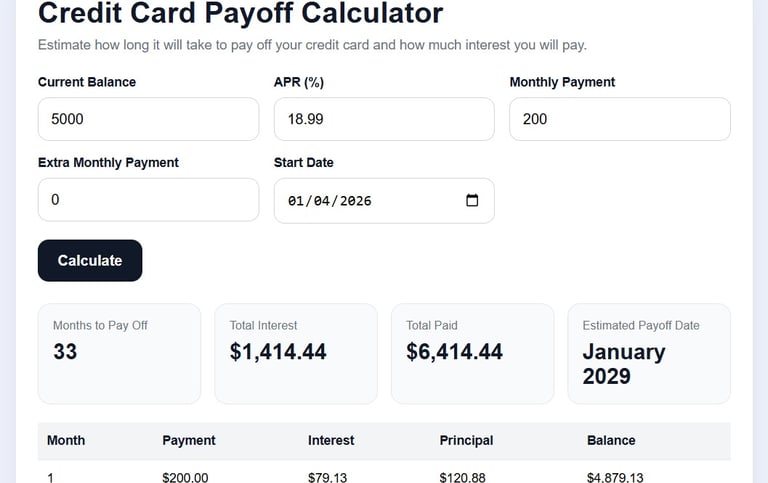

Try This: Minimum Payment Calculator

Want to see how your minimum payment is calculated?

👉 Use our Credit Card Minimum Payment Calculator to:

Estimate your minimum monthly payment

See how much goes to interest

Understand how little reduces your balance

This gives you a clear picture of why progress can feel slow.

Compare It With a Payoff Strategy

Minimum payments keep you in debt.

But increasing your payments changes everything.

👉 Try your numbers in a payoff calculator to see:

How long it takes to become debt-free

How much interest you can save

How to Break Free From Minimum Payments

1. Pay More Than the Minimum

Even an extra $50–$100/month can:

Reduce years off your debt

Save thousands in interest

2. Use a Strategy (Avalanche or Snowball)

Avalanche → Pay highest interest first (saves money)

Snowball → Pay smallest balance first (builds motivation)

3. Track Your Progress

Using calculators helps you:

Stay motivated

See real progress

Make smarter financial decisions

4. Avoid Adding New Debt

Try to:

Limit new spending

Focus on reducing your current balance

Frequently Asked Questions

Is paying the minimum bad?

Not always short-term, but long-term it keeps you in debt and increases total interest.

Why is my balance not going down?

Because most of your payment is going toward interest, not the principal.

How can I pay off debt faster?

Pay more than the minimum and use tools to plan your repayment strategy.

Final Thoughts

Minimum payments are designed to keep you paying — not to help you get out of debt.

If you want to take control:

Understand how your payments work

Use calculators to plan

Pay more whenever possible

👉 Small changes can lead to big results over time.

ClearEveryday

Free Loan & Debt Repayment Calculator

Estimate monthly payments, interest costs, and payoff timelines in seconds.

Link

© ClearEveryday 2026. All rights reserved.

About

For informational purposes only — not financial advice