No Signup Required • Instant Results • 100% Free Tools

Snowball vs Avalanche: Which Debt Strategy Works Best in 2026?

Compare the Debt Snowball and Debt Avalanche methods to find the best way to pay off debt in 2026. Learn which strategy saves more money vs. which builds more motivation.

Rachel

5/3/20263 min read

In 2026, debt feels heavier than ever.

With interest rates staying high, even small balances can feel like they’re barely moving — no matter how much you pay.

So choosing a debt strategy isn’t just about numbers anymore.

It’s also about how you stay consistent without burning out.

Most people end up choosing between two methods:

Debt Snowball (focus on small wins)

Debt Avalanche (focus on saving money)

One helps your mindset.

The other helps your wallet.

But which one actually works better right now?

The Quick Comparison

1. Debt Snowball: When You Need Momentum

The debt snowball method keeps things simple.

Instead of focusing on interest rates, you list your debts from smallest to largest balance.

How it works

Pay minimums on all debts

Put extra money toward the smallest one

Once it’s paid off → move to the next

Why it works

The biggest benefit isn’t financial — it’s psychological.

When you pay off a small debt quickly, you get a real sense of progress.

That feeling matters more than people think.

When this method makes sense

The snowball method is a good fit if:

You feel overwhelmed by multiple debts

You’ve struggled to stay consistent before

You need to see progress quickly

In 2026, where money stress is high, momentum can be more valuable than perfection.

2. Debt Avalanche: When You Want to Save More

The avalanche method takes a more strategic approach.

Instead of balances, you focus on interest rates.

How it works

List debts from highest interest to lowest

Pay minimums on everything

Put extra money toward the highest-interest debt

Why it works

This method reduces how much interest you pay over time.

That means:

More of your money goes toward your balance

You can become debt-free faster (mathematically)

When this method makes sense

The avalanche method is ideal if:

You have high-interest credit cards

You’re focused on saving money long-term

You’re disciplined enough to stay consistent

With current interest rates, this method can save you hundreds or even thousands over time.

So… Which One Should You Choose in 2026?

There’s no “perfect” answer — it depends on where you are right now.

👉 Choose Snowball if:

You feel stuck or discouraged

You need quick wins to stay motivated

You want a simple, easy system

👉 Choose Avalanche if:

You have high-interest debt

You want to reduce total interest

You’re focused on long-term savings

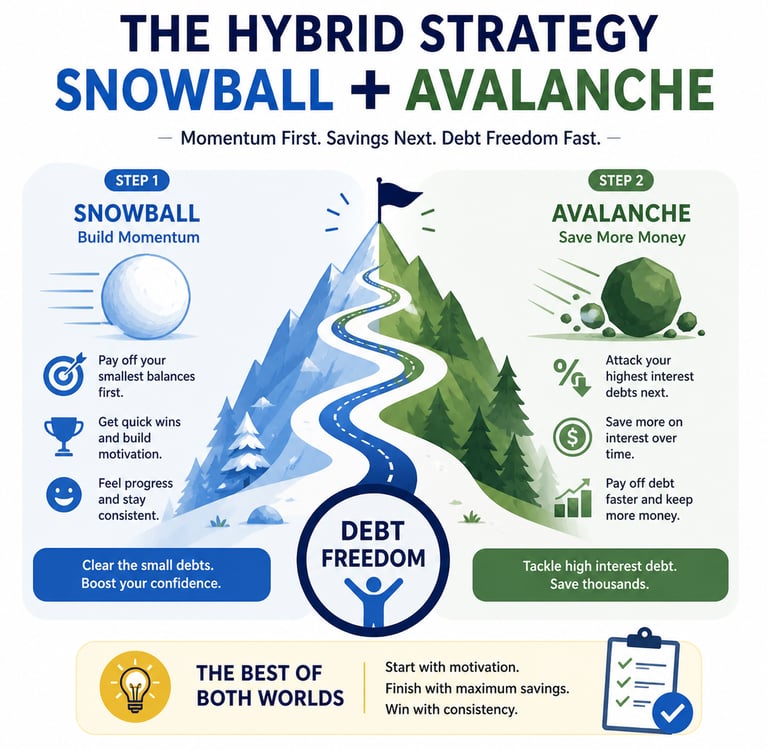

💡The Hybrid Strategy (What Most People Actually Do)

A lot of people don’t stick to just one method — and that’s completely okay.

A practical approach is:

Step 1: Start with Snowball

Pay off 1–2 small debts to clear mental pressure

Step 2: Switch to Avalanche

Once you’ve built momentum, focus on high-interest debt

This gives you:

Early motivation

Long-term savings

👉 It’s often the most realistic approach.

Ready to See Your Numbers?

The best way to decide is to look at your own situation.

Try:

Seeing your numbers clearly can make the decision much easier.

The Bottom Line

Both methods work.

The only method that doesn’t work is the one you can’t stick to.

If motivation is your biggest challenge → Snowball

If interest is your biggest problem → Avalanche

What matters most is consistency over time.

Rachel’s Note: Debt is personal. Don't let "math nerds" tell you the Snowball is wrong if it's the only thing keeping you motivated. Your mental health is a financial asset, too.

ClearEveryday

Free Loan & Debt Repayment Calculator

Estimate monthly payments, interest costs, and payoff timelines in seconds.

Link

© ClearEveryday 2026. All rights reserved.

About

For informational purposes only — not financial advice