No Signup Required • Instant Results • 100% Free Tools

Debt Consolidation Calculator: How Much Can You Save on Interest?

Use our debt consolidation calculator to estimate monthly payments, compare interest savings, and plan your payoff strategy. Take control of your debt today.

DEBT CONSOLIDATION

Rachel

3/26/20262 min read

Managing multiple debts can feel overwhelming — different balances, due dates, and high interest rates quickly add up.

A debt consolidation calculator helps you simplify everything into one loan and see how much you could save before making a decision.

Try the Debt Consolidation Calculator

Before we break it down, calculate your numbers:

👉 Use our Debt Consolidation Calculator

👉 Try our Loan Repayment Calculator

👉 Estimate with our Personal Loan Calculator

What Is a Debt Consolidation Calculator?

A debt consolidation calculator is a tool that helps you:

Combine multiple debts into one payment

Estimate your new monthly payment

Compare total interest costs

See your payoff timeline

👉 It gives you a clear financial picture before committing to a new loan.

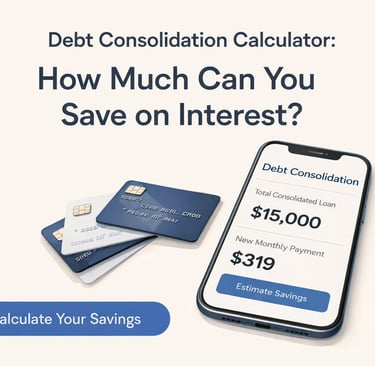

Example: Before vs After Consolidation

Before Consolidation:

Credit Card 1: $5,000 at 22%

Credit Card 2: $4,000 at 20%

Personal Loan: $6,000 at 15%

👉 Total Debt: $15,000

👉 Monthly Payments: ~$520

After Consolidation:

New Loan: $15,000 at 10% (5 years)

👉 Monthly Payment: ~$319

👉 Interest Savings: Thousands over time

💡 Even a small drop in interest rate can lead to significant savings.

How Much Can You Save?

Your savings depend on:

Your current interest rates

Your new loan rate

Your loan term

👉 The bigger the difference in interest rates, the more you save.

Calculate Your Savings Now

Don’t guess — calculate it instantly:

👉 Use our Debt Consolidation Calculator to:

Estimate your monthly payment

Compare interest costs

View your payoff timeline

Benefits of Debt Consolidation

1. Lower Monthly Payments

Combining debts can reduce your total monthly cost.

2. Lower Interest Rates

Especially if your credit score has improved.

3. Simpler Finances

One payment. One due date. Less stress.

When Debt Consolidation Is NOT a Good Idea

Debt consolidation isn’t always the best option.

Avoid it if:

The new interest rate is higher

There are high fees

You plan to keep using credit cards

👉 It only works if you stop adding new debt.

How Long Does It Take to Pay Off Consolidated Debt?

Typical loan terms:

3 years → Higher payments, less interest

5 years → Balanced option

7 years → Lower payments, more interest

Debt Consolidation vs Balance Transfer

Frequently Asked Questions

Does debt consolidation hurt your credit?

It may cause a small, temporary drop due to credit checks. However, consistent payments can improve your score over time.

What credit score do I need?

Most lenders require at least 600+, but better rates are usually offered to those with 700+ credit scores.

Can I consolidate with bad credit?

Yes, but interest rates may be higher. It’s important to compare options carefully.

Plan Your Debt-Free Strategy

👉 Use these tools to take control:

Credit Card Payoff Calculator

Final Thoughts

A debt consolidation calculator helps you make smarter financial decisions before taking on a new loan.

When used correctly, consolidation can:

✔ Lower your monthly payments

✔ Reduce financial stress

✔ Save money on interest

👉 The key is to calculate first — and choose the right strategy.

ClearEveryday

Free Loan & Debt Repayment Calculator

Estimate monthly payments, interest costs, and payoff timelines in seconds.

Link

© ClearEveryday 2026. All rights reserved.

About

For informational purposes only — not financial advice