No Signup Required • Instant Results • 100% Free Tools

Debt Avalanche Method: The Smartest Way to Pay Off Debt Faster

Pay off debt faster and save on interest with the debt avalanche method. Learn how it works and start building a smarter repayment plan today.

DEBT-FREE GUIDES

Rachel

5/1/20263 min read

If you’re serious about paying off debt as efficiently as possible, the debt avalanche method is one of the smartest strategies you can use.

Unlike other methods that focus on motivation first, this approach focuses on saving the most money on interest — helping you become debt-free faster in the long run.

If you’ve ever felt like your debt isn’t going down even though you’re making payments, this method can help you understand why — and fix it.

What Is the Debt Avalanche Method?

The debt avalanche method is a strategy where you focus on paying off the debt with the highest interest rate first, while continuing minimum payments on all other debts.

Once that debt is paid off, you move to the next highest interest rate — and continue until everything is cleared.

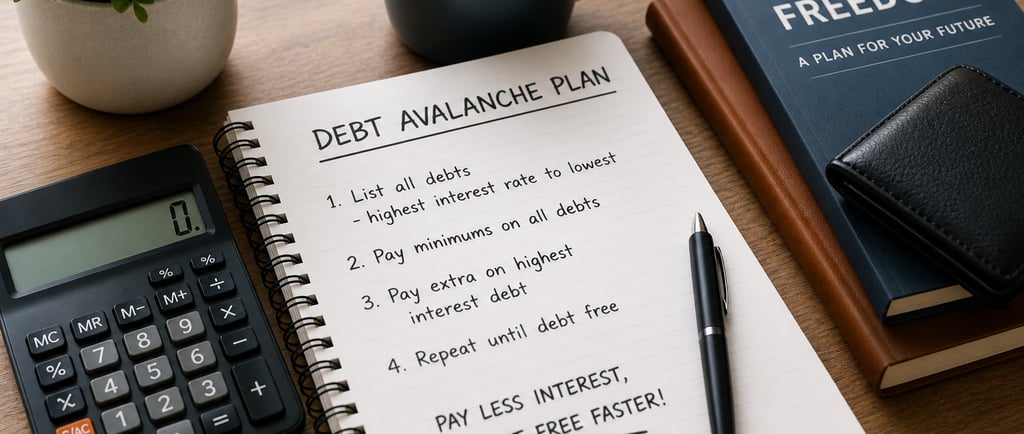

How It Works (Step-by-Step)

Step 1: List all your debts

Write down all your debts and order them by interest rate (highest to lowest).

Example:

Credit card – 22%

Personal loan – 12%

Car loan – 6%

Step 2: Pay minimums on everything

Keep all your accounts in good standing by paying the required minimum on each.

Step 3: Focus on the highest interest debt

Put any extra money toward the debt with the highest interest rate.

This reduces how much interest you’re being charged over time.

Step 4: Move to the next debt

Once the highest-interest debt is gone, take that payment and apply it to the next one.

This creates momentum — while still saving money on interest.

Why the Avalanche Method Works

The biggest advantage of this method is simple:

✔ You save more money

High-interest debt (like credit cards) costs you the most over time. Paying it off first reduces total interest paid.

✔ You get out of debt faster (mathematically)

Because less money is lost to interest, more of your payments go toward the actual balance.

✔ It’s efficient and strategic

This method is ideal if you want to optimise your money and reduce long-term costs.

Real-Life Example

Let’s say you have:

$1,000 credit card at 20%

$2,000 loan at 10%

$3,000 car loan at 5%

You have an extra $150 per month.

Using avalanche:

Pay minimums on all debts

Put extra $150 toward the 20% debt

👉 This reduces the fastest-growing debt first

Once that’s gone:

Move to the 10% loan

Then the 5% loan

👉 Result: you pay less interest overall

Avalanche vs Snowball (Quick Comparison)

Avalanche = highest interest first (saves money)

Snowball = smallest balance first (builds motivation)

👉 Avalanche is better for saving money

👉 Snowball is better for staying motivated

The best method? The one you can stick with consistently.

When the Avalanche Method Is Best

This method works best if:

You want to minimise interest costs

You’re disciplined and consistent

You don’t need quick emotional wins to stay on track

If you’re focused on efficiency, this is a great choice.

Simple Tips to Make It Work

Always pay minimums on time

Focus extra money on the highest interest debt

Avoid adding new debt

Track your progress monthly

Common Mistakes to Avoid

❌ Ignoring interest rates

❌ Spreading extra payments across all debts

❌ Losing consistency

Remember — focus is what makes this method effective.

Final Thoughts

The debt avalanche method is all about working smarter with your money.

It may not feel as motivating at the start, but over time, it can save you a significant amount in interest and help you become debt-free faster.

If your goal is efficiency and long-term savings, this method is a powerful strategy to follow.

FAQs

Is the avalanche method better than snowball?

It’s better for saving money on interest, but not always easier to stick with.

Can I switch methods later?

Yes. Many people start with snowball and move to avalanche later.

Does this work with all types of debt?

Yes — credit cards, loans, and other debts.

How much extra should I pay?

Any extra amount helps — consistency matters more than size.

🔗 Related Tools

ClearEveryday

Free Loan & Debt Repayment Calculator

Estimate monthly payments, interest costs, and payoff timelines in seconds.

Link

© ClearEveryday 2026. All rights reserved.

About

For informational purposes only — not financial advice