No Signup Required • Instant Results • 100% Free Tools

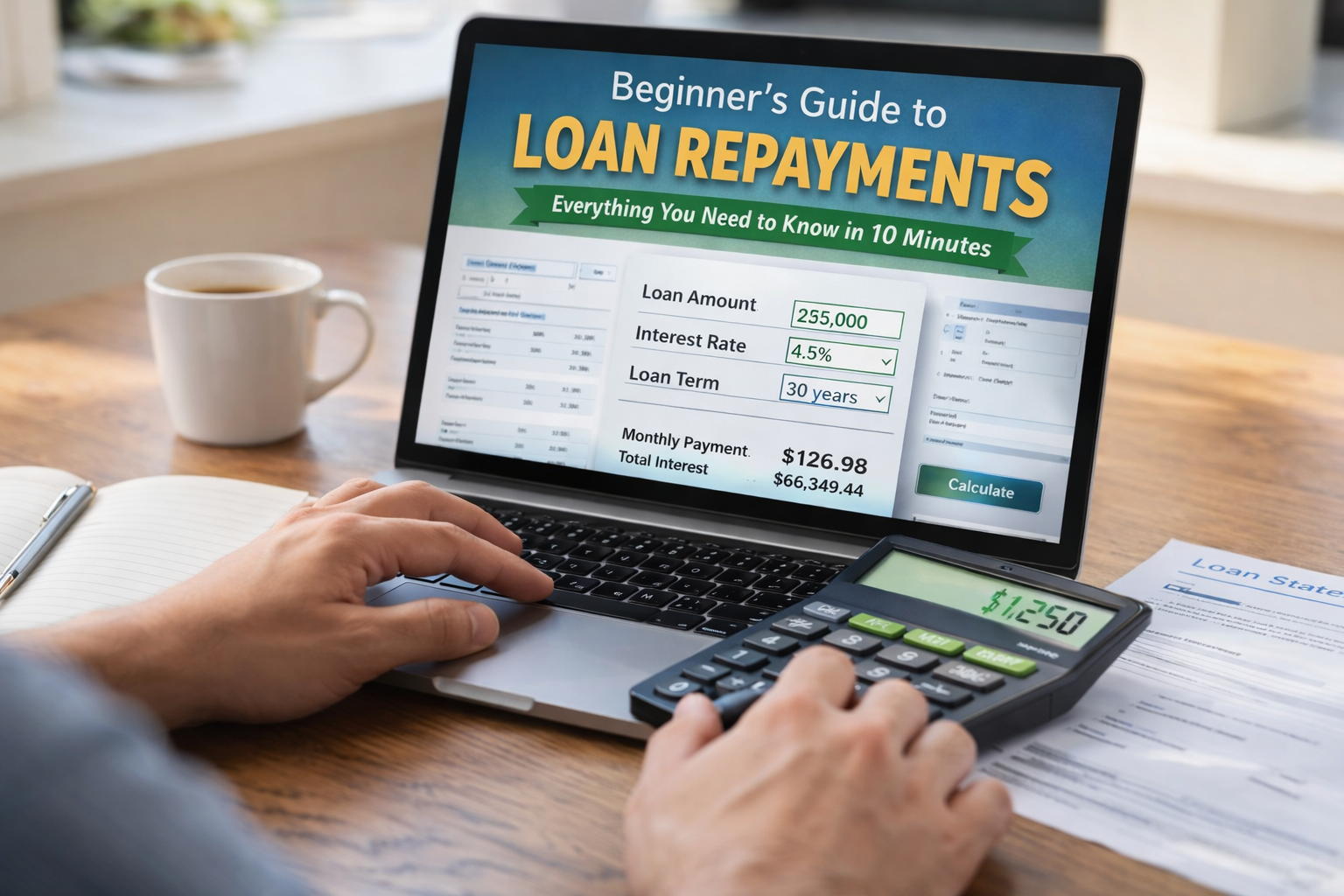

Beginner’s Guide to Loan Repayments: Everything You Need to Know in 10 Minutes

Learn how loan repayments work in minutes. Discover how interest adds up, how to reduce your payments, and simple strategies to pay off debt faster using easy calculator tools.

DEBT-FREE GUIDES

Rachel

4/6/20262 min read

If you have a home loan, car loan, personal loan, or credit card balance, understanding how repayments work is one of the fastest ways to take control of your finances.

Even small changes—like paying a little extra each month or choosing a shorter loan term—can save you thousands in interest and help you become debt-free sooner.

This guide explains everything in simple terms, so you can confidently use a loan calculator and make smarter decisions.

1) The 3 Numbers That Control Your Repayment

Every loan repayment is based on three key factors:

Loan amount (Principal): The amount you borrowed (or still owe)

Interest rate (APR): The yearly cost charged by the lender

Loan term: How long you take to repay the loan (e.g., 3, 5, or 30 years)

👉 Simple rule:

Higher loan + higher rate + longer term = more interest paid

2) Monthly Payment vs Total Cost (Big Difference)

Many people focus only on the monthly payment—but that’s not the full picture.

Here’s what actually matters:

Monthly repayment: What you pay regularly

Total interest: The extra money paid to the lender

Total cost: Loan amount + interest (plus fees if any)

⚠️ A longer loan term may feel easier monthly—but can cost you significantly more over time.

3) How Interest Really Works

Loan interest is calculated based on your remaining balance.

Early in the loan → more of your payment goes to interest

Later in the loan → more goes to principal (your debt)

👉 This is why paying extra early has the biggest impact.

4) Smart Ways to Pay Off Your Loan Faster

Try these strategies using a calculator to see real results:

A) Pay Extra Each Month

Even an extra $25–$100/month can:

Shorten your loan term

Reduce total interest significantly

B) Switch to Biweekly Payments

If allowed, this can result in one extra payment per year, helping you pay off faster.

C) Choose a Shorter Loan Term

Higher monthly payments

Much lower total interest

D) Refinance to a Lower Rate

A small drop in interest rate can save thousands—just check for fees before switching.

5) Credit Cards: The Minimum Payment Trap

Credit cards often have the highest interest rates.

If you only pay the minimum:

It can take years (or decades) to pay off

Most of your money goes to interest

👉 Use a credit card calculator to compare:

Fixed monthly payments (e.g., $200/month)

Adding extra each month

Payoff time and total interest

6) When Debt Consolidation Helps (and When It Doesn’t)

A debt consolidation calculator is useful if you have multiple debts.

It may help you:

Lower your monthly payments

Reduce total interest

Simplify everything into one payment

⚠️ But be careful—consolidation can backfire if:

The new loan term is much longer

You continue using credit cards after consolidating

7) Your 10-Minute Loan Check (Do This Today)

Use this quick routine:

Enter your loan details (balance, rate, term)

Note your monthly payment and total interest

Add a small extra payment (start with 1–5%)

Compare how much time and interest you save

If you have multiple debts, test consolidation options

Why This Matters

Understanding your loan isn’t complicated—but ignoring it can cost you thousands.

By simply testing different scenarios, you can:

Pay off debt faster

Save money on interest

Feel more in control of your finances

Final Takeaway

You don’t need to be a finance expert to make smarter decisions.

Start by using a calculator to test:

Extra payments

Shorter loan terms

Lower interest rates

Debt consolidation options

Small changes today can lead to big financial wins tomorrow.

Related Tools on ClearEveryday

ClearEveryday

Free Loan & Debt Repayment Calculator

Estimate monthly payments, interest costs, and payoff timelines in seconds.

Link

© ClearEveryday 2026. All rights reserved.

About

For informational purposes only — not financial advice