No Signup Required • Instant Results • 100% Free Tools

Debt Snowball Method: The Simple Way to Finally Pay Off Your Debt

The debt snowball method is a simple strategy to pay off debt by focusing on your smallest balances first and building momentum.

DEBT-FREE GUIDES

5/1/20263 min read

If you’re feeling overwhelmed by debt, you’re not alone.

Trying to pay off multiple balances at once can feel confusing and frustrating — especially when it seems like you’re making payments but not getting anywhere.

That’s where the debt snowball method comes in.

It’s one of the simplest and most motivating ways to pay off debt, especially if you need quick wins to stay consistent.

In this guide, we’ll walk you through exactly how it works, why it’s effective, and how to start — even if you’re on a tight budget.

What Is the Debt Snowball Method?

The debt snowball method is a way of paying off debt by focusing on your smallest balance first, while continuing minimum payments on everything else.

Once the smallest debt is paid off, you move to the next smallest — and so on.

As you go, your payments “snowball” into larger amounts, helping you clear debts faster over time.

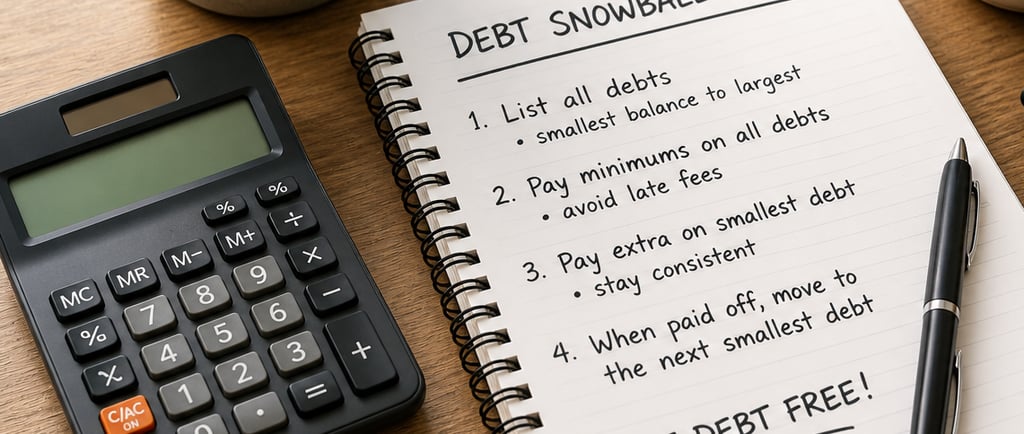

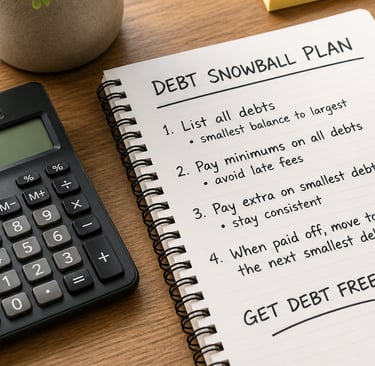

How It Works (Step-by-Step)

Step 1: List all your debts

Write down all your debts from smallest to largest balance (ignore interest rates for now).

Example:

$500 credit card

$1,200 personal loan

$3,000 car loan

Step 2: Pay minimums on everything

Make sure you’re paying the minimum required amount on all debts to avoid penalties.

Step 3: Focus on the smallest debt

Put any extra money you can toward the smallest balance.

Even small amounts help — consistency matters more than size.

Step 4: Roll payments into the next debt

Once the smallest debt is paid off, take that payment and add it to the next one.

This is where the “snowball” effect starts.

Why the Snowball Method Works

The biggest reason this method works isn’t just financial — it’s psychological.

✔ Quick wins keep you motivated

Paying off your first small debt gives you a sense of progress.

✔ It builds momentum

Each paid-off debt frees up more money to attack the next one.

✔ It simplifies your focus

Instead of juggling everything, you focus on one goal at a time.

Real-Life Example

Let’s say you have:

$500 debt (minimum $50)

$1,500 debt (minimum $75)

$3,000 debt (minimum $100)

You have an extra $100 per month.

Month 1:

Pay minimums on all

Put extra $100 toward the $500 debt

👉 That debt gets paid off faster

After it’s paid:

You now have $150 ($50 + $100)

👉 Apply that to the next debt

This keeps growing — just like a snowball rolling downhill.

Snowball vs Avalanche (Quick Note)

You might hear about another method called the avalanche method.

Snowball = smallest balance first

Avalanche = highest interest first

The avalanche method can save more on interest…

But the snowball method is often easier to stick with — and consistency is what actually gets you debt-free.

When the Snowball Method Is Best

This method works best if:

You feel overwhelmed by multiple debts

You need motivation to stay consistent

You’ve struggled to stick to other plans

If mindset is your biggest challenge, snowball is a great choice.

Simple Tips to Make It Work

Start small — don’t wait for “perfect timing”

Automate minimum payments

Put any extra cash (even $10–$20) toward your smallest debt

Celebrate small wins — they matter

Common Mistakes to Avoid

❌ Ignoring minimum payments

❌ Adding new debt while paying off old ones

❌ Giving up too early

Remember — this method works over time, not overnight.

Final Thoughts

The debt snowball method isn’t about being perfect.

It’s about building momentum, staying consistent, and finally feeling like you’re making progress.

If you’ve been feeling stuck with debt, this could be the simple system that helps you move forward.

Start with one small step — and let it build from there.

FAQs

Is the debt snowball method the fastest way?

Not always mathematically, but it’s one of the most effective for staying consistent.

Can I do this with low income?

Yes. Even small extra payments can build momentum over time.

Should I stop using credit cards?

It’s best to avoid adding new debt while paying off existing balances.

What if my debts are very large?

Start with the smallest anyway — the progress helps you stay motivated.

🔗 Related Tools

ClearEveryday

Free Loan & Debt Repayment Calculator

Estimate monthly payments, interest costs, and payoff timelines in seconds.

Link

© ClearEveryday 2026. All rights reserved.

About

For informational purposes only — not financial advice